A documented lived experience sits inside a longer American story: Black people can meet the standard, present the paperwork, and still find that access remains conditional.

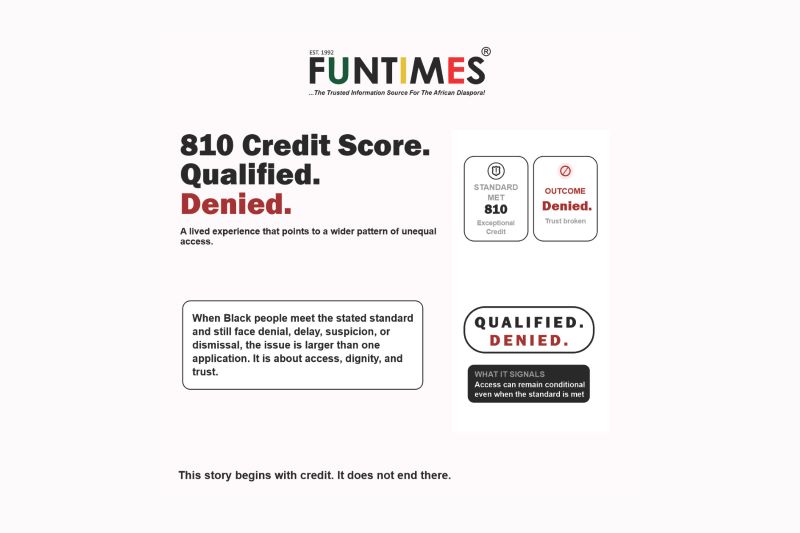

An 810 credit score is supposed to mean something.

So is a six-figure income.

In the language of modern finance, those markers signal discipline, capacity, and low risk. They suggest a person who has done what the system asked: built strong credit, earned steadily, and stayed within the rules.

And yet the answer was still no.

That is the 810 Paradox.

This is not fiction. It is a lived experience with documentation. And that matters because stories like this are often dismissed as exaggeration until the paperwork appears. In this case, the paperwork exists. The denial is real. The question is what it means.

At one level, lenders will say this is not unusual. Citi notes that a credit-card denial can happen for many reasons, including debt-to-income ratio, recent inquiries, too much available credit, or even application errors, and says applicants must receive an adverse action notice explaining the reason within 30 days. Chase similarly says applicants can have a good credit score and still be denied because approval decisions involve more than the score alone.

That explanation deserves to be acknowledged.

But it does not end the conversation.

Because the 810 Paradox is not really about whether one lender can list a reason. It is about a deeper and more troubling question: What does it mean when Black people meet the stated standard and still experience access as conditional?

That question is not new. It sits inside a long history of unequal treatment in credit and lending. The Equal Credit Opportunity Act makes it illegal to discriminate in any aspect of a credit transaction. The CFPB says that includes refusing credit if a person qualifies, discouraging someone from applying, offering worse terms than a similarly qualified applicant receives, or closing an account on prohibited grounds.

So the issue is not whether discrimination is forbidden on paper. It is whether it continues in practice.

There is evidence that it does.

The Federal Reserve’s research on mortgage lending found that minority applicants tend to have lower algorithmic approval rates even in race-blind automated underwriting systems, showing how disparities can persist even when race is not explicitly named in the decision. Bankrate, citing that research, notes that minority applicants tend to have lower credit scores, higher leverage, and lower automated approval rates. That does not prove every denial is discriminatory. It does show that historic inequality can remain embedded inside supposedly neutral systems.

The pattern extends beyond mortgages.

In 2024, the CFPB released a pilot study on small-business lending that found Black entrepreneurs received less encouragement to apply and were more often steered toward alternative products, including personal credit cards and home equity loans, compared with white testers who had similar or weaker business credit profiles. And in October 2024, the Justice Department announced that Citadel Federal Credit Union agreed to pay over $6.5 million to resolve allegations that it had redlined predominantly Black and Hispanic neighborhoods in and around Philadelphia.

That matters here because it answers a familiar objection.

The objection is that these are isolated experiences, unfortunate but individual. The record suggests otherwise.

What repeats is not always the exact act. What repeats is the structure: the standard is said to be objective, the process is said to be neutral, and yet the burden of friction, suspicion, discouragement, or denial keeps landing in familiar places.

That is why the 810 Paradox lands so hard. Have you, or someone you know experienced this denial? Share your story.

It compresses an old reality into one sharp contradiction: elite score, strong income, denial anyway. And the problem is larger than credit cards.

This pattern shows up in housing, insurance, business contracting, customer service, and retail. It appears anywhere Black people can arrive fully qualified and still sense that the welcome is uncertain. The qualifications may be present. The systems may look modern. The language may sound technical. But access can still feel conditional.

That is also why the conversation about Africa is changing.

At the sovereign level, African institutions have begun pushing for an Africa Credit Rating Agency, arguing that the continent has long been judged through external frameworks that do not fully reflect its realities. The African Union says the effort is meant to provide fair, transparent, African-owned ratings. Chatham House has pushed back, arguing that an Africa-only ratings agency will not solve the problem if borrowers still need to compete in global capital markets.

That debate matters because it mirrors the deeper issue beneath the 810 story: who gets to define risk, credibility, and worth?

From a single consumer application to sovereign borrowing, the same tension appears. People and places can do everything the system says they should do and still find themselves judged through standards that do not fully trust them.

So no, the 810 Paradox should not be watered down by broader context.

It should be sharpened by it.

The documented lived experience is the hook. The history, law, enforcement actions, and recurring disparities are the frame. Together, they support a harder question for financial institutions and for any business seeking cultural access to Black communities:

Do you want Black attention and Black dollars, or do you also want to be accountable for how Black people are treated once they apply, enter, ask, spend, and seek service?

That is the real test.

And that is why the 810 Paradox is beyond one denial story. It is a story about American systems, modern polish, and an old problem that still knows how to survive.

Have a story like this?

FunTimes Magazine is gathering documented and lived experiences involving denial, discouragement, profiling, or unequal treatment across credit, housing, insurance, business services, retail, and customer experience. Click here to share your story.

Are you a business serious about accountability?

FunTimes works with qualified partners seeking credible engagement with African Diasporacommunities through trust, relevance, and measurable follow-through. Partner with us.

Dr. Eric John Nzeribe is the Publisher of FunTimes Magazine and has a demonstrated history of working in the publishing industry since 1992. His interests include using data to understand and solve social issues, narrative stories, digital marketing, community engagement, and online/print journalism features. Dr. Nzeribe is a social media and communication professional with certificates in Digital Media for Social Impact from the University of Pennsylvania, Digital Strategies for Business: Leading the Next-Generation Enterprise from Columbia University, and a Master of Science (MS) in Publication Management from Drexel University and a Doctorate in Business Administration from Temple University.