Photo by Meshack Emmanuel Kazanshyi

No one likes the tax man, for he comes with his shovel to dig deep into the revenue bag and take what he or she believes is due, while leaving the taxpayer arguing over what is left. While many would argue over how much taxes they are required to pay, no one would dispute that taxes are vital in how economies are run, more so as they are required by the Government to meet its social contract with the citizens.

In Nigeria, on January 1, 2026, the recently introduced Nigeria Tax Acts, 2025, will come into effect. While this new act has generated a lot of controversy based on concerns of the excessive tax burden on citizens, lack of accountability for previous taxes on the part of the government, as well as the endemic corruption that has seen politicians live lavish lifestyles while the citizens live in penury. The bigger concern is understanding what the new tax reform Act means and how it affects citizens.

Nigeria Tax Acts, 2025

In June 2025, the Nigerian president signed four bills into law. They include the Nigeria Tax Act (NTA), the Nigeria Tax Administration Act (NTAA), the Nigeria Revenue Service Act (NRSA), and the Joint Revenue Board Act (JRBA). Collectively they all make up the Nigeria Tax Acts.

The New Act, which takes effect from January 1, 2026, is aimed at overhauling the tax framework of the country, making it more effective, broadening the tax base, and streamlining compliance across the board, increasing revenue generation, driving economic growth, and enhance tax administration across the three levels of government (federal, state and local government).

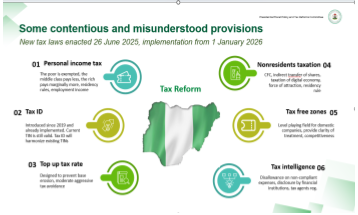

Highlights of the Nigeria Tax Acts

Image Source: Powerpoint presentation by Taiwo Oyedele, Chairman of the Presidential Fiscal Policy and Tax Reforms Committee, 26 September, 2025

Several changes were introduced in the New Tax Act that address how tax administration will be handled in the country from 2026. In a report by Baker Tilly International titled Nigeria’s 2025 Tax Reform Acts Explained: Key Changes, Business Impacts, and Compliance Strategies, specific points highlighting the changes in the Nigerian Tax Act were outlined.

Below are some of the important highlights of the new act.

| Tax Reform Area | Summary of Change |

| Corporate Tax Relief for Small Businesses | Small companies (gross turnover ≤ ₦50m and fixed assets ≤ ₦250m) are exempt from CIT, CGT, and the 4% Development Levy. |

| Capital Gains Tax (CGT) Overhaul | CGT rate for companies has increased from 10% to 30%, aligning it with the corporate tax rate. Indirect offshore share transfers are now taxable. |

| Development Levy (4%) | A new 4% levy on assessable profits replaces multiple levies (TET, NASENI, PTF, and IT Levy). |

| Personal Income Tax (PIT) Reform | More progressive PIT bands. Incomes ≤ ₦800,000 per year are now tax-exempt. The top marginal rate increased to 25% for high earners. |

| Economic Development Incentive (EDI) | Replaces Pioneer Status. Eligible businesses receive a 5% annual tax credit on qualifying capex for up to 5 years, with carry-forward provisions. |

| Minimum Effective Tax Rate (ETR) | Large companies (₦50bn+ turnover or part of an MNE with €750m+ global revenue) must pay a minimum 15% ETR. A top-up tax applies if paid ETR is lower. |

| VAT Input Recovery & Zero-Rating | VAT at 7.5% is retained, with an expanded zero-rated goods list (e.g., food, books, and medical supplies). Input VAT on services and capex is now fully claimable. |

| Mandatory VAT E-Invoicing & Fiscalisation | All registered businesses must adopt e-invoicing and real-time VAT systems aligned with FIRS technology protocols. |

| Definition of Residency for PIT | PIT now applies to the worldwide income of Nigerian residents. This is defined to include those with economic/family ties during the year. |

| Tax Compliance Technology | Comprehensive digitization of compliance systems across all taxes, including stamp duties and VAT, is required with automated reporting. |

| Stamp Duty on Agreements and Contracts | Stamp Duty (SD) on agreements and contracts has been well defined, classed and exemptions explicitly stated.Also, the rate is now fixed at N1,000 and is no more ad-valorem at 1%.Additionally, the following have been exempted from SD:• Agreement and contracts whose value is less than ₦1,000,000.• Employees’ agreement and contracts, e.g., labourers, artificers, manufacturers or menial servants.• Contracts that are made for or relate to the sale of any goods, wares or merchandise, including hire purchase agreement. |

| Taxation of Lottery and Gaming Trade or Business | The NTA provided for a broad taxation of profit of gaming companies.According to the Act, gaming includes gambling, wagering, video poker, roulette, craps, bingo, slot or gaming machine, drawings or other games of chance conducted by any person. |

| Tax Ombud & Dispute Resolution | The new Tax Ombud Office and upgraded Tax Appeal Tribunal offer structured channels for taxpayer complaints and dispute resolution. |

Source: https://www.bakertilly.ng/insights/nigerias-2025-tax-reform-acts-explained

What these changes mean for individuals and businesses

The new Nigeria Tax Act is sure to affect individuals and businesses immediately it becomes effective from next year. Understanding how it will do so would help with better financial planning going into the new year.

Individuals

The new tax act makes a few modifications to personal income tax, taking into consideration several factors to make it more progressive.

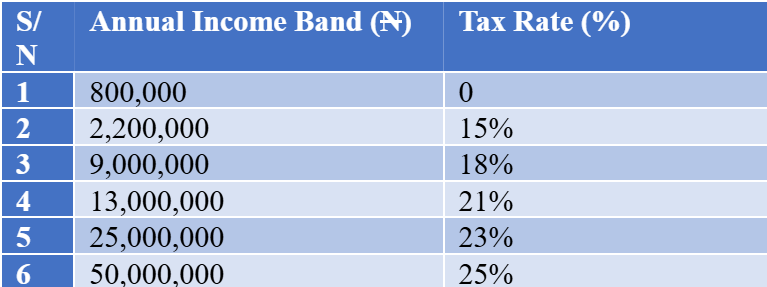

Revised Personal Income Bands: The new tax rate provides that low-income earners who earn an annual taxable profit of N800,000 or less will be exempted from paying personal income tax. This measure considers the current minimum wage in the country and ensures that the burden of taxation is not imposed on Nigeria’s lowest earners. Increased marginal rates, however, will apply for high-income earners with an increase from 15% to 25% for different income levels.

As noted in a report titled The Nigeria Tax Act1 (NTA), 2025 by KPMG, “The revised structure introduces a more progressive tax system by providing significant relief to low-income earners and ensuring that higher income earners contribute a larger share of their income”

Non-Resident and Resident Employment Income: Non-residents (foreigners) working in the country will only be taxed on the employment income earned in the country, where their duties are performed, and not in their country of residence. Resident individuals, however, will be taxed on their income. Providing clarity on the issue of residency, the act notes that an individual is considered resident if the individual has spent 183 days or more in the country, owns or maintains a permanent home or has a significant economic or family tie within the taxable year.

PAYE and WHT Streamlined: The act also requires standard documentation of employee benefits and ensures uniform deduction and remittance of monthly withholding tax (WHT) and pay-as-you-earn (PAYE) by companies with the revenue agency mandated to ensure compliance. Also, interest earned by individuals on short-term securities like treasury bills, bonds, etc., will now be subject to WHT.

Companies

The new tax act also addresses some aspects affecting the operation of companies in the country.

Recognition of MSMEs: To encourage the growth of MSMEs within the country and improve compliance, the act raises the requirements for the classification of MSMEs. As noted in the KPMG report, “Section 56 of the Act stipulates that small companies (companies that have gross turnover of ₦100m or less per annum and with total fixed assets not exceeding ₦250m) and large companies be subjected to tax at 0% and 30% respectively. The 30% rate for large companies can be reduced to 25% effective from a date as may be determined in an Order issued by the President on the advice of the National Economic Council.”

Development Levy: Nigerian companies will be required to pay a development levy of 4% which will be applied to the companies’ taxable profits prior to deduction for depreciation and losses. This development is only applicable to large companies with small businesses and non-resident companies exempted.

Economic Development Incentive (EDI): Tax credits of 5% per annum are offered to eligible companies looking to invest in capital expenditure within a five-year period. If a company has unused tax credits, such credits can be carried over for another 5 years. Any credit not used within the timeline will automatically expire.

Capital Gains Tax (CGT) and Indirect Transfer of Shares: The New Tax Act has also increased the tax on CGT from 10% to 30%. Capital Gains Tax is the profit earned after a capital asset is disposed of. It is on that profit that CGT tax will be charged. Also, tax exemption on the sale of shares for Nigerian companies has been increased from N100 million to N150 million.

Effective Tax Rate (ETR): Nigerian companies that belong to a multinational group with an estimated turnover of EUR750 million and above and an annual turnover upwards of N50 billion will be subject to a 15% ETR on their net income.

How These Rules Will Impact Savings, Spending, Remittances etc.

Several other changes have been implemented in the new Tax Act to help lessen the burden on citizens. For example, the value-added tax rate of 7.5% which had always been applied to the purchase of essential items like food, road transport services, tuition fees, and pharmaceutical products, has been removed. That means that the extra charges for items purchased by individuals at stores will no longer apply, thereby saving people a considerable amount of money at the end of the year.

Individuals can comfortably save funds in their accounts without worrying about the tax man deducting from their savings, as the only funds to be taxed are the interest on savings, not the principal amount.

No remittance tax has been introduced in the new Act, so individuals can comfortably send money to their loved ones and pay only the standard service fee, as applicable.

Compliance Steps Nigerians Need to Take

As the New Nigerian Tax Act comes into effect, Nigerians are concerned about several things, chief of which is the need to ensure proper financial planning of their finances. In providing insights on what to do, the professional services firm PricewaterhouseCoopers (PwC) offers six suggestions of what companies and businesses can do as the Act comes into effect in 2026.

| S/N | 6 Top Things Companies and Businesses Need to Do | |

| 1 | Become Aware | Sensitise management – Organise sensitisation workshops for relevant board committees and executive management onthe impact of the reforms on your business. Empower your people – Train and upskill staff to ensure seamless adoption of new tax laws in specific roles and processes that are impacted. |

| 2 | Assess | Carry out a holistic impact analysis – Proactively assessthe corporate structure, operational, financial and compliance implications arising from the tax laws. This can also include considering the impact on supply chains, commercial arrangements such as acquisitions anddivestments, incentive regimes and so on. |

| 3 | Articulate | Reframe tax strategy – Reframe your tax strategy to align with the commercial goals of the business. More will be expected from the tax function to protect business value amidst the various changes arising from the new laws or technology changes such as by VAT fiscalisation. Set up a Tax Risk Register – Implement a living risk register to continuously identify, monitor, and control tax risks and opportunities that have been triggered by the reforms in real time. |

| 4 | Operationalise and implement | Update compliance processes – Taxpayers will need to update their compliance processes in line with the tax laws. For example, taxpayers will need to update their systems to cater for new rates, revised compliance obligations and filing requirements, information sharing, claims for input VAT etc. Execute your implementation plan – Achieve tasks in yourimplementation plan effectively and efficiently in line with your strategic objectives. Leverage technology – Update the logic in accounting software and ERP to align with the new rules. Ensure processes and technology align to ensure end-to-end compliance and prepare for changes such as e-invoicing. Optimise tax governance & management frameworks- Evaluate, expand, or eliminate tax functions and processes for effectiveness and efficiency, closing compliance gaps and embedding robust internal controls. |

| 5 | Engage | Engage stakeholders – Determine a communication strategyand protocol for key internal and external stakeholders. Some examples include: Shareholders – ROI impact, Employees – PAYE impact, Customers – e-invoicing processes, Vendors – KYC and validation, Tax authorities – rulings on new risks, host communities etc., to ensure a smooth transition and adoption process. |

| 6 | Monitor | Stay updated – Regularly monitor official communications, information circulars or regulations from the government authorities issued pursuant to the Tax laws. Manage change – Apart from training and upskilling, there should be a deliberate change management plan to drive behaviour, review and monitor the transition and adoption of the new rules. |

For Individuals

| S/N | Top Things Individuals Must Do | |

| 1 | Obtain Your Tax Identification Number | TIN is now required to operate a bank account. National identification numbers will now serve as TIN. For individuals without any, it is necessary that they visit the nearest state revenue agency to get one or register to get their NIN. |

| 2 | Tax Filing | For individuals working in organizations, it is expected that your company will file your annual returns. For small businesses and sole proprietorships, having your annual return filed is essential to ensure you do not run foul of the law. |

| 3 | Review Your Income Band | Individuals should endeavour to review their annual income to better understand where they fall within the taxable income bracket. This would also help with better financial planning after individual PAYE has been deducted. |

| 4 | Stay Updated | Regularly read and monitor official correspondence from recognized government tax agencies to stay up to date on new developments. |

Note of Caution

Companies, businesses, individuals must bear in mind that non-adherence to the new tax law comes with penalties. Below are some of the applicable penalties for tax defaulters.

- Any taxable person who knowingly files inaccurate or incomplete tax returns is liable to an administrative fine of N100,000 in the first month of default and N50,000 for consecutive months should the default continue.

- The Act also makes provision for penalties for taxpayers who fail to keep proper records of all transactions and revenue necessary for accessing the taxable income.

- The Act also extends penalties to businesses or companies who refuse to grant access to tax authorities to deploy appropriate technology for tax assessment.

- When there is failure to remit the tax within the required period, the taxpayer will be required to pay a 10% default fee of the total amount payable.

- Failure to deduct tax, fraud with respect to stamp duties, impersonation of an authorized officer, counterfeiting of documents, among others attract a fine of N1 million to N10 million. Failure to comply with the Tax Administration Act attracts a fine of N20 million and N2 million for each subsequent day with the possibility of six months’ jail time should the default continue.

- Penalties against a corporate body shall be enforced against the entity’s directors, managers, secretaries, partners or anyone in like manner as the person who committed the offence, unless proven that the offence committed was done without the knowledge of the said person.

Okechukwu Nzeribe works with the Onitsha Chamber of Commerce, in Anambra State, Nigeria, and loves unveiling the richness of African cultures. okechukwu.onicima@gmail.com